The Trans Mountain Pipeline Generates Billions

A detailed look at how the Canada Development Investment Corporation navigated a record quarter of revenue and debt restructuring.

On the first day of May in 2024, a quiet but monumental shift occurred in the Canadian energy landscape. After years of political strife, ballooning budgets, and construction delays that seemed to stretch toward the horizon, the Trans Mountain Expansion Project finally opened its valves for commercial business. For the engineers and laborers on the ground, it was the end of a grueling physical marathon. But for the accountants in Toronto and Ottawa, the real work was just beginning.

By the autumn of 2025, the financial impact of that day had solidified into hard numbers. The Canada Development Investment Corporation, the Crown corporation tasked with managing this colossal asset, released its third-quarter report for the period ending September 30, 2025. The document reveals a dramatic reversal of fortune. For the first time in recent memory, the state-owned entity is not merely absorbing costs but generating massive operational cash flow. The Trans Mountain Pipeline has begun to pay its way, bringing in billions in revenue while simultaneously undergoing one of the most complex debt restructuring exercises in Canadian corporate history.

The narrative emerging from the ledger is one of stabilization. The bleeding stopped when the oil started flowing. Yet, beneath the headline profit figures lies a intricate web of government loans, interest rate maneuvering, and new mandates that have transformed this Crown corporation from a temporary holder of assets into a central pillar of federal economic strategy.

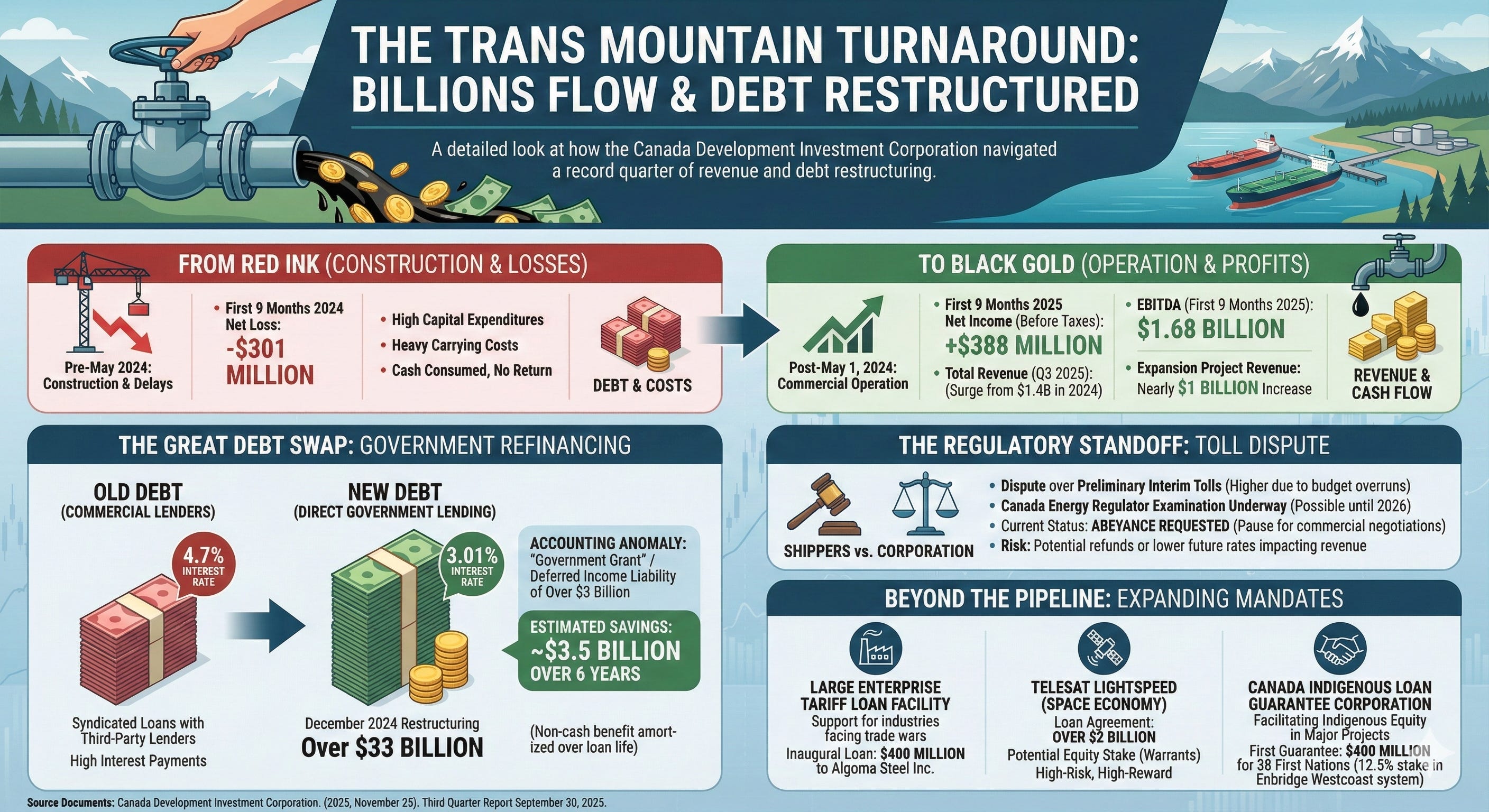

From Red Ink to Black Gold

To understand the magnitude of the shift, one must look at the stark contrast between the years of construction and the era of operation. In the first nine months of 2024, the corporation bled money, posting a net loss of $301 million. It was a period defined by capital expenditures and the heavy carrying costs of a project that was consuming cash without generating a return.

Fast forward one year. For the same nine-month period in 2025, the corporation posted a net income before taxes of $388 million. The driver of this turnaround was the Trans Mountain Pipeline itself. Total consolidated revenue for the period surged to $2.3 billion, a staggering increase from the $1.4 billion recorded the previous year. The expansion project alone accounted for nearly a billion dollars of that jump, as the increased throughput capacity allowed more crude to reach the Westridge Marine Terminal and global markets.

The operational reality of the pipeline is now visible in the cash flow. In the first nine months of 2025, the corporation generated $1.68 billion in earnings before interest, taxes, and depreciation. This is the engine the government hoped to build—a cash-generating machine capable of servicing the massive debt incurred to build it. However, revenue is only half the equation. The expenses involved in running such a massive piece of infrastructure have also climbed. Operating costs, salaries, and administrative expenses rose as the workforce expanded to support the new system, but these increases were eclipsed by the sheer volume of tariff revenue pouring in from shippers.

The Great Debt Swap

While the oil revenue grabs the headlines, the true financial engineering took place in the back offices of the Department of Finance and Export Development Canada. The construction of the expansion project left the Trans Mountain Corporation with a mountain of debt, much of it financed through syndicated loans with third-party lenders at commercial rates. As long as those loans existed, a significant portion of the pipeline’s new revenue would be eaten up by interest payments.

In a decisive move to protect the asset’s value, the federal government stepped in to restructure the entire liability profile. In December 2024, the government replaced the corporation’s third-party financing with direct government lending. This was not a simple stroke of a pen but a massive refinancing operation involving over $33 billion in loans. The objective was clear: lower the cost of capital.

The report details the mechanics of this swap. The interest rate on the massive acquisition and construction facilities was slashed from 4.7 percent to 3.01 percent. For a debt pile of this magnitude, a 1.7 percent reduction translates into hundreds of millions of dollars in annual savings. The report estimates that this restructuring will reduce financing costs by approximately $3.5 billion over the next six years.

This move created an accounting anomaly known as a “government grant.” Because the government is lending money to its own corporation at rates below what the private market would charge, international accounting standards require this benefit to be recorded. The corporation recognized a “deferred income” liability of over $3 billion, essentially booking the value of the cheap money as a non-cash benefit that will be amortized over the life of the loans. It is a subsidy by another name, designed to ensure that the Trans Mountain Pipeline appears financially viable on paper while allowing the government to retain ownership without immediate insolvency risks.

The Regulatory Standoff

Despite the influx of cash and the favorable loan terms, the corporation faces a brewing storm with its customers. The oil companies that use the pipeline—the “shippers”—are currently locked in a dispute over the tolls charged to transport their product. The preliminary interim tolls, which came into effect when the expansion opened, are higher than the industry expected, driven by the project’s budget overruns.

The Canada Energy Regulator is the arbiter of this dispute. A regulatory examination is currently underway, a process that could drag on into early 2026. The stakes are incredibly high. If the regulator decides the tolls are too high, the corporation could be forced to issue refunds or lower its future rates, damaging the revenue streams required to pay back the taxpayer.

Recognizing the danger of a protracted legal battle, the corporation and the shippers have hit the pause button. In October 2025, the Trans Mountain Corporation requested an “abeyance”—a suspension of the regulatory process—to allow time for commercial negotiations. The hope is that a negotiated settlement can be reached outside the hearing room, providing certainty for both the pipeline operator and the oil producers. Until that deal is signed, the revenue figures, while impressive, remain subject to regulatory gravity.

Beyond the Pipeline

While the Trans Mountain Pipeline dominates the balance sheet, the Canada Development Investment Corporation has quietly evolved into a Swiss Army knife for federal economic policy. The third-quarter report reveals a flurry of activity in subsidiaries that have nothing to do with oil transport, highlighting the corporation’s expanding mandate.

One of the most significant developments is the activation of the Large Enterprise Tariff Loan facility. Created in response to aggressive trade policies and tariffs from the United States, this program is designed to support large Canadian industries caught in the crossfire of global trade wars. In September 2025, the corporation announced its inaugural loan under this facility: a $400 million lifeline to Algoma Steel Inc. This transaction signals that the corporation is now the government’s primary vehicle for bailing out strategic industries facing geopolitical headwinds.

Simultaneously, the corporation is venturing into the final frontier. Through a new subsidiary, it has executed a loan agreement worth over $2 billion to support Telesat Lightspeed, a low-earth orbit satellite project. This deal includes the acquisition of warrants, giving the taxpayer a potential equity stake in the satellite company. It is a high-risk, high-reward play, placing the Crown corporation directly into the competitive space economy.

The Fading Giant and New Alliances

As new mandates rise, old ones quietly fade. The Canada Hibernia Holding Corporation, which manages the federal interest in the offshore Hibernia oil field, reported a decline in fortunes. Net crude oil revenue dropped by 16 percent compared to the previous year, driven by falling global oil prices and a natural decline in production. Hibernia, once a crown jewel of Canadian energy, is entering its twilight years. While it continues to generate cash, its role as a primary revenue driver is diminishing, eclipsed by the massive volumes moving through the Trans Mountain system.

In contrast, the corporation’s newest venture, the Canada Indigenous Loan Guarantee Corporation, is just finding its footing. Mandated to help Indigenous groups acquire equity in major projects, it issued its first guarantee in July 2025. This $400 million guarantee facilitated a deal for thirty-eight First Nations in British Columbia to acquire a 12.5 percent stake in Enbridge’s Westcoast pipeline system. This marks a structural shift in how the government approaches economic reconciliation, moving from direct transfers to financial backstopping that allows Indigenous communities to become owners of energy infrastructure.

The Long Road Ahead

The picture that emerges from the third quarter of 2025 is one of a government entity in transition. The Canada Development Investment Corporation is no longer just a holding tank for assets the government wants to sell. It has become an active manager of a diverse and complex portfolio that spans heavy crude, steel manufacturing, space telecommunications, and Indigenous finance.

The Trans Mountain Pipeline remains the sun around which these other planets orbit. Its successful commercialization has stopped the financial hemorrhaging, but the mountain of debt remains. The government has bought time and stability through its refinancing efforts, swapping high-interest commercial risk for long-term public liability. The bet is that the pipeline will run full, the tolls will hold, and the global demand for Canadian oil will persist long enough to pay down the $33 billion mortgage.

For now, the valves are open, the ships are sailing, and the ledger is finally black. But in the volatile world of energy markets and trade wars, stability is often just a pause between storms.

Source Documents

Canada Development Investment Corporation. (2025, November 25). Third Quarter Report September 30, 2025.