The Lost Billions of the Asia Pacific Trade Boom

In 1997 experts warned that relying on the United States would cost us dearly while the Asian tigers roared. We are still paying the price.

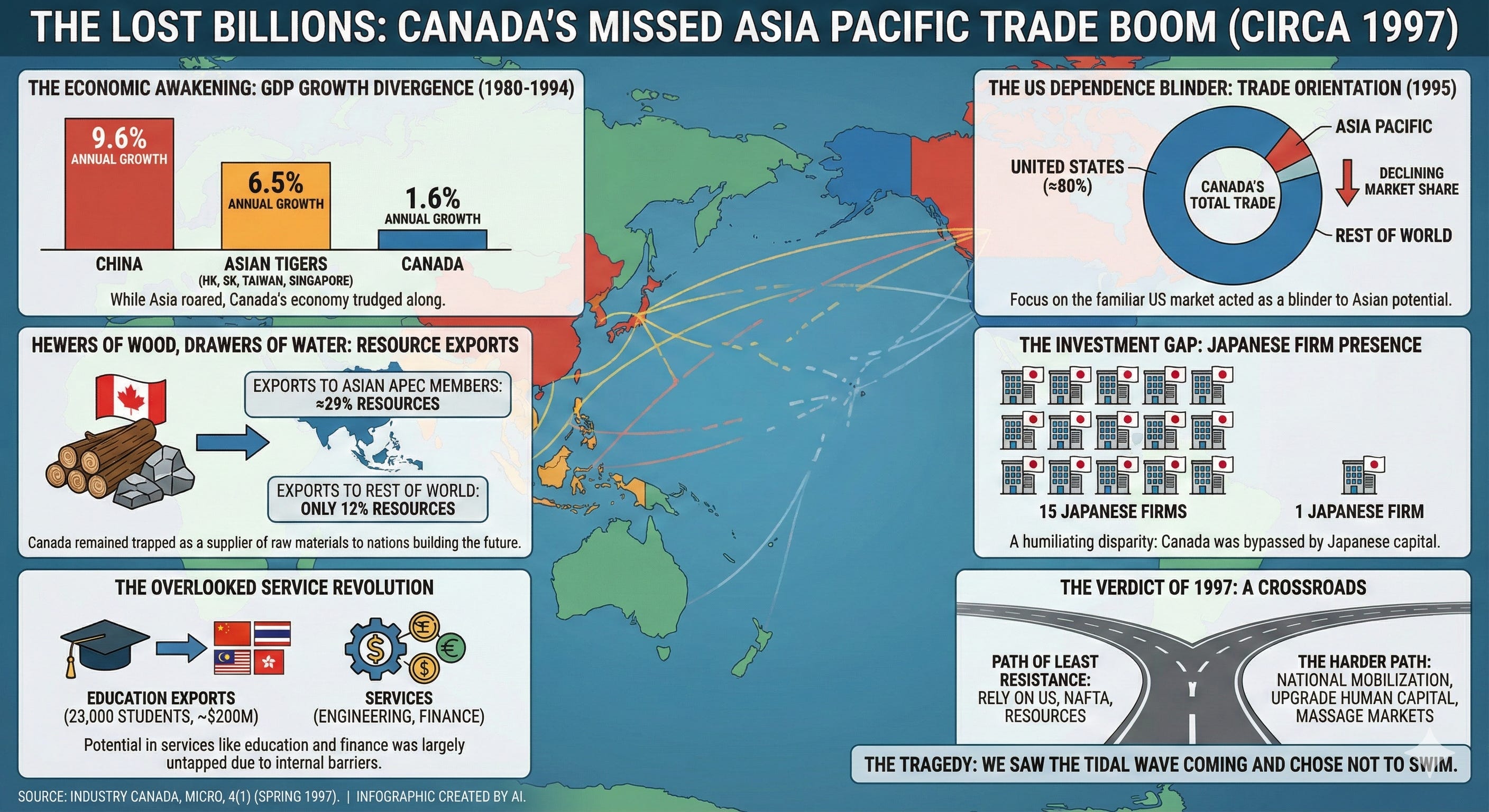

It was the spring of 1997 and the global economic tectonic plates were shifting with a violence that few in Ottawa seemed to fully comprehend. While the ink was drying on the North American Free Trade Agreement and Canadian businesses were looking comfortably south toward the United States, a massive awakening was occurring across the ocean. The Asia Pacific trade boom was not merely a trend. It was a fundamental reordering of the world’s wealth, and the warning signs were flashing red: Canada was missing the boat.

The numbers circulating through Industry Canada at the time told a haunting story of lost potential. Real Gross Domestic Product per capita in the People’s Republic of China had averaged a staggering growth rate of 9.6 percent annually between 1980 and 1994. The newly industrialized economies of Hong Kong, South Korea, Taiwan, and Singapore were close behind at 6.5 percent. In stark contrast, Canada’s economy had trudged along at 1.6 percent. The world was witnessing the most rapid economic expansion in human history, yet Canada’s commercial eyes remained fixed on the familiar American market.

This was the pivotal moment when the “Pacific Century” truly began to dawn. The experts of the day knew that more than one third of the world’s population resided in the Asia Pacific region, a consumer base nearly six times larger than the European Union. Yet, despite this explosive potential, Canada’s share of these dynamic markets was not just small. It was slipping.

The Hewers of Wood and Drawers of Water

The diagnosis of the Canadian condition in 1997 was stark. Walid Hejazi and Daniel Trefler, analyzing the trade patterns of the era, uncovered an uncomfortable truth about the Canadian economy. Even after accounting for the country’s vast natural wealth, Canada had unusually high levels of natural resource exports. Approximately 29 percent of Canada’s total exports to the Asian members of the Asia Pacific Economic Cooperation were resources, compared to only 12 percent to the rest of the world.

We were selling raw logs and minerals to nations that were busy building the future.

The irony was sharp. Many of the nations in the region were themselves resource exporters, competing directly with Canadian products. While forecasts suggested that the Asian tigers would eventually become massive consumers of resources, the immediate reality was that Canada was failing to move up the value chain. East Asia was flooding the world with low-end manufactures, driven by aggressive industrial policies, while Canada remained trapped in its historical role as a supplier of raw materials.

This reliance on resources masked a deeper structural weakness. Canada’s trade orientation had shifted dramatically toward the United States following the Free Trade Agreement. By 1995 almost 80 percent of Canadian trade was with the US. This continental focus acted as a blinder. While Canadian exports to the US surged, the country’s market share in the dynamic Asian economies was eroding. We were trading comfort for growth, ignoring the reality that the Asian economies were expected to expand by 7 percent annually for the next decade compared to a sluggish 2.5 percent for North America.

The Investment Gap and the Fifteen to One Ratio

If the trade numbers were worrying, the investment figures were alarming. Japan was the undisputed economic heavyweight of the region in 1997, dominating world industries and exporting capital across the globe. Yet Canada was failing spectacularly to attract this flow of yen.

The disparity was humiliating. For every fifteen Japanese firms that established a presence in the United States, only one set up shop in Canada. We were being bypassed. Even within the country, the benefits were unevenly distributed, with only Ontario ranking among the top twenty North American locations for Japanese companies.

The flow of money going the other direction was equally anemic. Canadian direct investment in the region was weak. In 1980 Canadian investment represented a meager 0.6 percent of total inward foreign direct investment in the newly industrialized economies. By 1992 it had crept up to 2.5 percent, but in China—the engine of future growth—Canada’s share of foreign investment had actually declined from 0.5 percent to 0.4 percent.

Economists Keith Head and John Ries looked at the situation and saw a dangerous temptation for Canadian provinces. To attract fleeting Asian capital, local governments might be tempted to engage in damaging subsidy wars. They pointed to the “Newfoundland solution” of offering thousands of dollars per job created. It was a race to the bottom that threatened to lower the economic welfare of the winning province, a desperate scramble for scraps rather than a coordinated national strategy to integrate with the Asian boom.

The Invisible Export and the Education Goldmine

While the resource and manufacturing sectors struggled to find their footing, a quieter revolution was taking place in the service sector. Lawrence Schembri argued that Canada held a comparative advantage that was being overlooked: its people and its institutions.

In the early 1990s, no fewer than 23,000 students from the Asia Pacific region were enrolled in Canadian postsecondary institutions. This was not just cultural exchange. It was big business. These students represented about $200 million in business service exports. Given the immense cultural value placed on education in Asian societies, this was a goldmine waiting to be tapped.

However, the barriers were internal. Postsecondary education was the jealously guarded domain of the provinces. Expanding this market required a level of coordination and deregulation that was politically difficult. Yet the potential was undeniable. Engineering, consulting, and financial services were poised for growth. The demand for services in Asia was outstripping the rest of the world, and Canada had the expertise in resource extraction and construction that the developing Asian giants desperately needed to build their infrastructure.

The banking sector also looked East with hungry eyes. John Chant noted that as income grew in Asia, the importance of financial systems would skyrocket. Canadian banks, having cut their teeth in the competitive markets of the US and Europe, were theoretically ready. But they faced a wall of regulation. Aside from Hong Kong and Japan, Asian banking systems were fortresses of protectionism. The hope was that Canadian banks would follow Canadian direct investment, but with investment so low, the banks were left waiting for a deregulation wave that was slow to break.

The Looming Shadow of the Internet

While economists debated trade flows and tariffs, a different kind of storm was gathering on the horizon, one that would eventually render physical distances irrelevant. In September 1996 Hal Varian, a visionary from the University of California, Berkeley, visited Industry Canada to speak about a burgeoning technology called the Internet.

At the time, the web was a chaotic frontier. Varian described a world where the “public” and “private” facets of the network were colliding. He warned of a future where critical decisions about digital infrastructure might be made prematurely by poorly informed policymakers. He predicted the rise of “cybercrime” and the inevitability of regulation, drawing parallels to the automobile industry.

Varian’s insights were prophetic. He foresaw a shakeout where only a few large telecommunications companies would survive to dominate the backbone of the internet. He spoke of the tension between privacy and the “nosiness” of corporations. This digital revolution was the unseen undercurrent of the trade conversation. The Asia Pacific boom would eventually be supercharged by the very information technologies Varian was analyzing, creating a globalized economy where information moved faster than cargo ships.

The Small Business Failure

The backbone of the Canadian economy has always been small and medium-sized enterprises. In 1996 these firms created two-thirds of all new private sector jobs. Yet when it came to the Asian economic miracle, Canadian small businesses were nowhere to be found.

Someshwar Rao and Ashfaq Ahmad found that while outward-oriented Canadian small businesses were competitive against their American counterparts, they were paralyzed by fear and lack of resources. Only 10 percent of these firms exported at all, and a microscopic 0.2 percent invested abroad. Their participation in the Asia Pacific region was negligible compared to larger firms.

The obstacles were formidable. Trade barriers, regulatory opacity, and investment restrictions in Asia raised the cost of doing business to levels that small firms simply could not absorb. Unlike a multinational corporation, a small manufacturer in Ontario could not afford to spread high entry costs over a massive volume of sales. They lacked the financing, the market knowledge, and the international managerial experience to navigate the complex cultural and political waters of the East.

This was a critical failure of policy. By leaving the Asian market to the resource giants and the multinationals, Canada was failing to cultivate the next generation of global exporters. The engines of domestic job growth were being cut off from the engine of global economic growth.

The Geopolitical Squeeze

Hovering over every trade statistic was the complex geopolitical dance between the United States and Japan. Wendy Dobson reviewed the simmering tensions between the world’s two largest economies and saw Canada caught in the crossfire.

The United States was aggressive, launching initiatives to pry open Japanese markets. Japan resisted. The impasse was dangerous for Canada because, in the eyes of Tokyo and Beijing, Canadians were often viewed as being “like” Americans. If a trade war erupted, or if Japan retreated into a defensive Asian trading bloc, Canada would be collateral damage.

There was a real fear that Japan might lead an exclusive Asian economic zone that would shut out North America. Conversely, the rise of Mexico as a low-cost manufacturing hub within NAFTA threatened to divert trade away from Asia, creating tension with Pacific partners. Canada was walking a tightrope. It needed to reduce its own trade barriers to Asian goods to prove it was a “fair trader,” while simultaneously relying on the US to break down the protectionist walls in Tokyo and Seoul.

The Verdict of 1997

As the spring of 1997 turned to summer, the consensus among the experts was clear but unsettling. The “Pacific Century” was not a slogan. It was a mathematical certainty. The Asian economies were on a trajectory to dominate global growth for decades.

Canada stood at a crossroads. The path of least resistance was to continue hugging the United States, relying on the easy commerce of NAFTA and the export of raw materials. The harder path required a national mobilization: a concerted effort by government and business to penetrate the difficult, distant, and culturally distinct markets of Asia.

It required upgrading the human capital base, as Australia was attempting to do, to move beyond simple resource extraction. It required government policies that “massaged” the market, taking lessons from the aggressive science and technology strategies of South Korea and Singapore. It required a shift in the national psyche from an Atlantic and continental focus to a truly Pacific outlook.

The warning was written in the data. If Canada did not establish a visible, aggressive presence in Asia, it would be relegated to the periphery of the global economy, a supplier of logs and rocks to the nations that were building the future. Looking back from the vantage point of history, the tragedy is not that we didn’t know what was happening. It is that we saw the tidal wave coming and chose not to swim.

Source Documents

Industry Canada. (1997, Spring). Micro, 4(1).